The Architecture of Member Understanding

Why Member-Based Institutions Need a Formal Discipline of Customer Technology

A member institution cannot steward what its architecture cannot understand.

This may become one of the defining technology challenges for superannuation funds, pension systems, mutual banks, health funds, cooperative insurers, credit unions, professional associations, and other member-based organisations over the next decade. These institutions have long described themselves through the language of trust, prudence, fiduciary responsibility, collective benefit, and member outcomes. Their legitimacy rests on the belief that they exist to serve people over time, often across some of the most consequential domains of human life: retirement, financial security, health, insurance protection, professional identity, community participation, and pooled economic resilience.

Yet the relationships through which these responsibilities are fulfilled are now increasingly mediated by technology.

Members encounter institutions through portals, apps, statements, call centres, campaigns, claims systems, advice tools, employer interfaces, chatbots, identity systems, digital forms, data-driven communications, automated workflows, and service platforms. Their needs are interpreted through data models. Their questions are routed through systems. Their behaviours are scored, segmented, measured, and sometimes predicted. Their consent is recorded somewhere. Their histories are distributed across records. Their vulnerabilities may be known by one part of the organisation and invisible to another. Their interactions generate signals that may or may not become usable institutional memory.

The relationship between a member and an institution is therefore no longer simply a matter of policy, product, governance, service, or communication. It is increasingly shaped by architecture.

This creates a problem that many member-based organisations are only beginning to confront fully. Their technology estates have often been assembled over many years around functions, channels, products, campaigns, regulatory requirements, service processes, and operational workflows. These systems may be individually capable. They may be modern in parts. They may include strong platforms, rich data environments, and significant digital investment. But they were not always designed as coherent architectures of member understanding.

The member experiences one organisation. The architecture often behaves like many.

This gap matters because member-based institutions are not ordinary transactional enterprises. Their relationships are long, episodic, regulated, trust-sensitive, economically consequential, and often socially significant. A superannuation fund may be connected to a person for forty or fifty years. A pension system may influence the dignity of retirement across an entire population. A health fund may become most visible during moments of vulnerability. A mutual insurer may be judged by the quality of its response when a household experiences loss. A credit union or mutual bank may carry a community promise that extends beyond the provision of financial products. A cooperative may depend on participation, identity, and shared value rather than simple consumption.

These are not relationships that can be governed well through fragmented technology.

The challenge is becoming more urgent because member institutions are being pushed simultaneously by several forces. Members expect greater relevance, continuity, responsiveness, and transparency. Regulators expect clearer evidence of fair treatment, outcomes, accountability, privacy, and governance. Boards expect productivity, efficiency, risk control, and strategic adaptability. Executives expect technology to reduce cost, improve service, personalise engagement, and unlock insight. AI capabilities now add another layer of pressure, promising automation, decision support, member assistance, and operational leverage while raising deeper questions about context, permission, explainability, and trust.

The temptation is to respond to these pressures with more technology: another platform, another data layer, another automation tool, another AI use case, another digital transformation program. In some cases, additional tools are necessary. But the central question is no longer whether member institutions possess enough technology. Many already possess more technology than their organisations can coherently govern.

The deeper question is whether their technology is organised around the relationship it is meant to serve.

This is the territory of Customer Technology.

Customer Technology can be understood as the formal management of the systems, data structures, platforms, interaction models, and governance mechanisms through which an organisation understands and acts in relation to the people it serves. In member-based institutions, Customer Technology becomes the architecture of member understanding: the discipline of designing and governing the technological capability through which members are recognised, remembered, supported, protected, engaged, and served over time.

This is different from simply having customer-facing systems. It is different from owning a CRM, a marketing automation platform, a contact centre system, a member portal, a data warehouse, an analytics environment, or a digital experience layer. Those tools may all be part of the estate. None of them, alone, constitutes the architecture of member understanding.

The distinction matters because technology now determines whether member institutions can scale relationship stewardship responsibly. It determines whether context can travel across channels, whether consent can be enforced consistently, whether member identity remains coherent, whether interactions become institutional learning, whether digital systems preserve continuity, whether AI can operate safely, and whether scale becomes operating leverage or operating drag.

In member-based institutions, Customer Technology is no longer a back-office concern. It is becoming a central condition of institutional performance.

The Distinctive Technology Problem of Member Institutions

Most customer technology disciplines emerged in commercial contexts where the dominant problems were acquisition, conversion, retention, service, personalisation, and growth. Retailers needed to understand customers well enough to sell more effectively. Banks needed to improve onboarding, cross-sell products, and manage service. Telecommunications companies needed to reduce churn and optimise channel interactions. Digital platforms needed to personalise experiences, increase engagement, and scale behavioural insight. Marketing technology, CRM, analytics, and service platforms evolved largely within these contexts.

Member-based institutions share some of these needs, but their deeper problem is different.

Their relationships often unfold over decades rather than campaign cycles. A superannuation fund’s relationship with a member may begin early in working life, pass through employment changes, family formation, contribution interruptions, advice needs, consolidation decisions, retirement planning, pension drawdown, and eventually estate or beneficiary considerations. The institution may interact with the member only occasionally, yet the consequences of the relationship accumulate continuously.

The relationship is also episodic. Members may remain silent for long periods and then suddenly require high-stakes support. A health fund member may engage lightly until a diagnosis, treatment decision, hospital admission, or family health event. An insurance member may interact minimally until a claim. A pension participant may ignore communications for years and then require guidance at retirement. A cooperative member may participate economically but only engage institutionally during moments of governance, dispute, change, or crisis.

This episodic quality creates a distinctive architectural requirement. The institution must preserve context even when interaction is infrequent. It must be able to re-enter the relationship with memory. It must recognise that long gaps between interactions are not empty; they are periods during which life circumstances change, trust may strengthen or decay, needs may emerge silently, and the member’s capacity to act may shift.

The relationship is also consequential. In many member institutions, decisions are not merely preferences. They affect retirement income, financial wellbeing, health access, insurance protection, family security, or community participation. This raises the standard for technology. Systems that support these relationships must be designed for clarity, auditability, explainability, consent, vulnerability awareness, and accountable decision-making. A poorly timed retail recommendation may irritate a customer. A poorly timed retirement nudge, claims intervention, insurance communication, or advice-adjacent message can create far more serious consequences.

The relationship is regulated. Superannuation, pensions, financial services, health, and insurance operate under demanding legal and fiduciary constraints. Technology must support these constraints at scale. Consent, privacy, disclosure, advice boundaries, record-keeping, complaint handling, fairness, accessibility, and member-outcome obligations cannot remain external policy concerns. They must be embedded in the architecture through which interactions occur.

The relationship is often mediated. Many member institutions do not have as direct a relationship with members as their membership numbers suggest. Employers, advisers, brokers, administrators, payroll systems, unions, comparison platforms, healthcare providers, outsourced contact centres, and digital intermediaries may all shape the member’s experience and interpretation of the institution. The formal member relationship may sit with the institution, while the practical relationship is distributed across an ecosystem.

Finally, the relationship is collective. In member-based organisations, individual engagement patterns can influence the collective economics of the system. Attrition, disengagement, poor participation, underuse of support, misunderstanding, and loss of trust can affect operating scale, risk pools, cost structures, service investment, and the collective value proposition available to the remaining member base. This makes the architecture of member understanding economically significant in a way that ordinary transactional customer systems often are not.

These characteristics create a different kind of technology problem.

A member institution does not simply need to know who clicked, who called, who opened, who converted, or who complained. It needs to understand how people move through long-term relationships with the institution; how context changes; how trust is built, damaged, or restored; how members interpret institutional action; how life events alter needs; how vulnerability emerges; how engagement relates to outcomes; and how technology can support responsible action without becoming intrusive, manipulative, or incoherent.

That is a profound architectural challenge.

The Inheritance Problem: Technology Built Around Functions

Most member institutions did not begin with a blank sheet of paper and design a unified architecture of member understanding. They inherited and accumulated technology over time.

Product systems were implemented to administer accounts, policies, investments, contributions, claims, or benefits. Service platforms were deployed to manage calls, cases, complaints, workflows, and resolution. Digital teams built portals, mobile apps, forms, and self-service tools. Marketing teams adopted campaign platforms, email systems, segmentation tools, journey builders, and personalisation engines. Data teams built warehouses, lakes, models, dashboards, and reporting environments. Risk and compliance teams implemented controls, registers, monitoring tools, and audit processes. Finance teams maintained cost and performance systems. Operations teams optimised throughput. Technology teams integrated what they could and stabilised what they had to.

Each layer made sense in its own context. The problem is that the member relationship cuts across all of them.

The result is often a technology estate that reflects the institution’s internal structure more than the member’s lived relationship. The architecture knows products, channels, cases, campaigns, events, transactions, permissions, and records. It may not know the member as a coherent evolving relationship.

A member might update information in one channel and still be treated as unknown in another. A vulnerability disclosed in service may not influence communication logic. A retirement intent captured in one interaction may not shape future engagement. A consent preference may be recorded but not consistently enforced across systems. A complaint history may be visible to one team and invisible to another. A member’s digital behaviour may trigger a campaign without reference to their recent service difficulty. A claims interaction may not become part of broader relationship understanding. A call centre agent may spend the first half of an interaction reconstructing context the institution should already possess.

These are not merely experience defects. They are symptoms of architectural fragmentation.

In earlier digital environments, this fragmentation often revealed itself as inconvenience. Members repeated themselves. Staff searched multiple systems. Communications were inconsistent. Service handoffs were clumsy. Campaigns were mistimed. Reports contradicted one another. Leaders struggled to obtain a single view of member behaviour.

Those problems remain important. But as member institutions become more automated, data-driven, and AI-enabled, fragmentation becomes more consequential. When systems act on incomplete context at scale, the institution does not merely appear inefficient. It may behave inconsistently, inappropriately, or irresponsibly.

Architecture becomes conduct.

This is why Customer Technology cannot be reduced to platform selection or system implementation. The deeper issue is not whether an institution owns modern tools. It is whether those tools collectively create a coherent capacity to understand, remember, decide, and act in relation to members.

A fragmented institution can buy excellent platforms and still fail to become more capable. It may simply automate fragmentation more efficiently.

Digital Experience Is Not Member Understanding

Over the past decade, many member institutions have invested substantially in digital experience. Portals have improved. Apps have become more usable. Forms have been simplified. Self-service has expanded. Digital messaging has become more sophisticated. Service channels have become more integrated. Member dashboards, calculators, educational tools, and online account management have improved significantly.

This progress matters. Poor digital experience creates friction, exclusion, cost, and distrust. A member who cannot find information, complete a form, understand a balance, submit a claim, update details, or access support is not being well served. Digital access is now a basic institutional obligation.

But digital access is not the same as institutional understanding.

A polished interface can sit on top of fragmented data. A well-designed app can display information without interpreting relationship state. A self-service tool can reduce calls while leaving members uncertain. A personalised message can use superficial variables while missing deeper intent. A seamless transaction can still fail to build trust. A dashboard can show balances, claims, policies, or contributions without helping the member understand what those facts mean for their life.

Digital experience often asks whether the member can complete an action. Customer Technology asks whether the institution understands the relationship in which that action occurs.

This distinction is especially important for member-based institutions because many of their most important outcomes do not happen within a single interaction. Retirement confidence, insurance adequacy, financial resilience, health participation, cooperative engagement, and trust in institutional stewardship develop across time. They are cumulative outcomes shaped by repeated encounters, absences, messages, decisions, moments of uncertainty, and interpretations of institutional behaviour.

A member may log in successfully and still not understand whether they are on track. A health fund member may complete a claim and still feel unsupported. A mutual bank member may use the app daily and still have little sense of the institution’s member-owned purpose. A pension participant may receive accurate information and still lack the confidence to act. A cooperative member may transact efficiently while becoming disengaged from governance and shared identity.

Digital systems can improve access without improving understanding. They can accelerate interaction without strengthening relationship. They can reduce human effort without increasing institutional intelligence.

The risk is that member institutions mistake digital modernisation for relationship capability.

This mistake is understandable because digital outputs are visible. Apps, portals, dashboards, chat interfaces, and automated communications create tangible evidence of progress. Architecture is less visible. Context models, identity resolution, consent structures, encounter records, decision logic, data lineage, governance workflows, integration patterns, and measurement frameworks are harder to see. Yet they often determine whether digital experience is truly meaningful or merely well-presented.

The member sees the interface. The institution must govern the architecture beneath it.

From Data to Context

Many member institutions now have more data than at any point in their history. They know balances, contributions, claims, policies, products, service events, call histories, complaint records, web visits, app logins, email opens, campaign responses, demographic attributes, transaction patterns, and sometimes external or inferred behaviours. Data warehouses, customer data platforms, analytics environments, reporting suites, and machine learning initiatives have expanded the institutional appetite for insight.

Yet data abundance does not guarantee relationship intelligence.

A record of what happened is not the same as understanding what it means. A contribution change may indicate a salary change, employer issue, life event, financial stress, strategic choice, or administrative error. A missed payment may indicate disengagement, hardship, confusion, or transition. A claim may be a routine transaction or a moment of acute vulnerability. A login pattern may indicate confidence, anxiety, comparison shopping, or confusion. Silence may indicate satisfaction, avoidance, low salience, or lack of trust.

The institution may know the event while misunderstanding the condition.

This is the difference between data and context.

Context gives data meaning in relation to the member’s circumstances, intent, permissions, history, vulnerability, life stage, and relationship state. Without context, technology can only react to signals. With context, it can support judgement.

Member institutions need to become much more serious about context because their relationships are long and consequential. A superannuation fund that knows a member is approaching retirement but does not understand their confidence, advice needs, spouse situation, debt, employment intentions, or anxiety may communicate accurately but inadequately. A health fund that knows a member has made claims but not how those claims relate to ongoing care needs may serve efficiently but incompletely. An insurer that sees policy changes without understanding vulnerability or household risk may miss opportunities for support or fairness. A mutual bank that sees declining engagement without understanding financial stress may treat a member as inactive when they are actually at risk.

The move from data to context is not merely an analytics challenge. It is an architectural challenge.

Where does context live? Who is allowed to use it? How is it created? How is it validated? How does it decay? How does it travel across channels? How is consent attached to it? How is sensitive context protected? How is it distinguished from inference? How does it influence service, communication, decisioning, escalation, and measurement? How does the institution avoid overreach, manipulation, or inappropriate personalisation?

These questions sit at the heart of Customer Technology.

The goal is not to create an omniscient institution. In member-based organisations, that would be both unrealistic and ethically dangerous. The goal is to create governed contextual capability: the ability to remember what should be remembered, forget what should not be retained, interpret what is relevant, protect what is sensitive, and act in ways that improve member outcomes and institutional trust.

This requires architectural maturity. It requires data models that represent relationships, not just transactions. It requires identity structures that recognise members across channels and life stages. It requires consent systems that are enforceable in practice. It requires interaction records that capture more than activity logs. It requires decision frameworks that distinguish service, education, marketing, advice, risk, and stewardship. It requires governance that can operate inside technology, not merely around it.

Context is the raw material of member understanding. Architecture determines whether that context becomes useful, responsible, and scalable.

When Scale Becomes Operating Drag

Scale is usually treated as one of the great advantages of member-based institutions. In superannuation, pensions, mutual insurance, health funds, cooperative banking, and other member systems, scale can reduce average cost, support stronger investment in capability, improve bargaining power, broaden service options, and expand the resources available to serve the collective membership.

Yet scale is only an advantage when the architecture beneath it is coherent.

Customer Technology determines whether scale becomes operating leverage or operating drag. A mature architecture allows institutions to reuse member context, preserve interaction memory, govern consent, coordinate channels, and deliver more consistent support at lower marginal cost. A fragmented architecture produces the opposite effect. It forces members to repeat themselves, staff to reconcile systems manually, teams to rebuild partial views of the member, and leaders to make decisions from incomplete evidence.

In small systems, these defects are irritating. In institutions serving millions of members, they become economic.

Poor Customer Technology multiplies the cost of misunderstanding. Every duplicated record, broken handoff, irrelevant communication, missing permission, stale profile, disconnected channel, and manual workaround carries a marginal cost. At scale, those costs compound. The institution becomes more expensive to operate, slower to change, harder to govern, and less capable of delivering the benefits that scale is supposed to provide.

This is one of the most important economic arguments for Customer Technology in member-based organisations. Technology is not simply a cost centre. It is the productive machinery through which relationship stewardship becomes scalable, repeatable, governable, and economically viable.

When that machinery is coherent, the institution gains several forms of leverage.

It gains context leverage: the ability to reuse member understanding responsibly across interactions, channels, and life stages. It gains governance leverage: the ability to enforce consent, escalation, risk controls, and outcome obligations consistently across the member base. It gains interaction leverage: the ability to make each encounter cheaper, more useful, more coherent, and more informative. It gains learning leverage: the ability for the institution to improve its understanding of members over time.

When the architecture is weak, the opposite occurs. The institution pays repeatedly to rediscover what it should already know. It pays through longer calls, duplicated communications, member frustration, manual reconciliation, remediation, compliance overhead, poor targeting, inconsistent decisions, slow change, and lost trust. It pays through technology programs that become more expensive because the underlying context and integration foundations are weak. It pays through AI initiatives that cannot scale safely because the data, permissions, and decision structures are not ready.

This is where Customer Technology economics become inseparable from member economics.

In a member-based organisation, inefficient architecture does not merely reduce enterprise productivity. It can dilute the collective advantage of membership itself. If scale should produce lower costs, better capability, stronger support, and more resilient services, then poor architecture can prevent those benefits from reaching the member base. The institution may be large, but the member may still experience fragmentation, repetition, irrelevance, and institutional amnesia.

Scale without coherent architecture can become a burden shared by the members the institution exists to serve.

That is why technology leaders in member institutions need an economic language beyond delivery cost, platform rationalisation, and operational efficiency. They need to ask whether their architecture improves the institution’s capacity to understand and serve members at lower marginal cost over time. They need to measure whether each encounter strengthens the next one, whether context reduces duplication, whether governance becomes easier to enforce, whether digital investments create reusable capability, and whether technology spend compounds into institutional intelligence.

A mature Customer Technology architecture creates an economic flywheel. Each encounter improves the institution’s understanding of the member. That understanding, governed responsibly, improves the next interaction, reduces duplication, strengthens relevance, lowers service cost, improves decision quality, and generates better evidence for future investment. Over time, the institution becomes not merely more digital, but more capable.

That is the economic promise of Customer Technology.

Encounter Anatomy: The Missing Primitive

If member institutions are to build architectures of understanding, they need to become more disciplined about the unit through which relationships actually unfold: the encounter.

Every meaningful interaction between a member and an institution has anatomy. Someone is involved. Something happens. There is a reason, a channel, a timing, a context, a permission boundary, an institutional response, and a consequence. The encounter may be a call, claim, login, advice discussion, contribution change, complaint, retirement inquiry, campaign response, educational session, chatbot exchange, employer-mediated update, or service escalation. It may be initiated by the member, the institution, an intermediary, a system, or a life event.

Too often, institutions treat encounters as operational events rather than relationship events.

A call is logged as a call. A campaign response is logged as a response. A form submission is logged as a transaction. A complaint is logged as a case. A claim is logged as a claim. A web visit is logged as behavioural data. Each record may be useful to the function that created it, but the broader relationship meaning can be lost.

Customer Technology requires a richer view.

An encounter should help the institution understand the member relationship more deeply. It should clarify intent, context, need, confidence, permission, risk, vulnerability, satisfaction, unresolved issues, and future relevance where appropriate. It should contribute to institutional memory. It should inform what happens next. It should be governed by clear rules about what can be retained, reused, inferred, escalated, or forgotten.

This is especially important because member relationships are episodic. If interactions are infrequent, each encounter carries more weight. The institution cannot afford to let meaningful context disappear into disconnected systems. A retirement inquiry should not be treated merely as a service event if it signals a life transition. A complaint should not be treated merely as a resolution workflow if it reveals a breakdown in trust. A claim should not be treated merely as a financial process if it signals vulnerability. A contribution change should not be treated merely as an administrative update if it suggests financial stress or changed employment circumstances.

Encounter intelligence is the foundation of relationship memory.

Without it, institutions remain trapped in activity records. They know what happened, but they do not consistently learn from what happened. Their systems record contact but fail to develop understanding. Their dashboards show volume but not meaning. Their channels operate, but their relationship architecture does not mature.

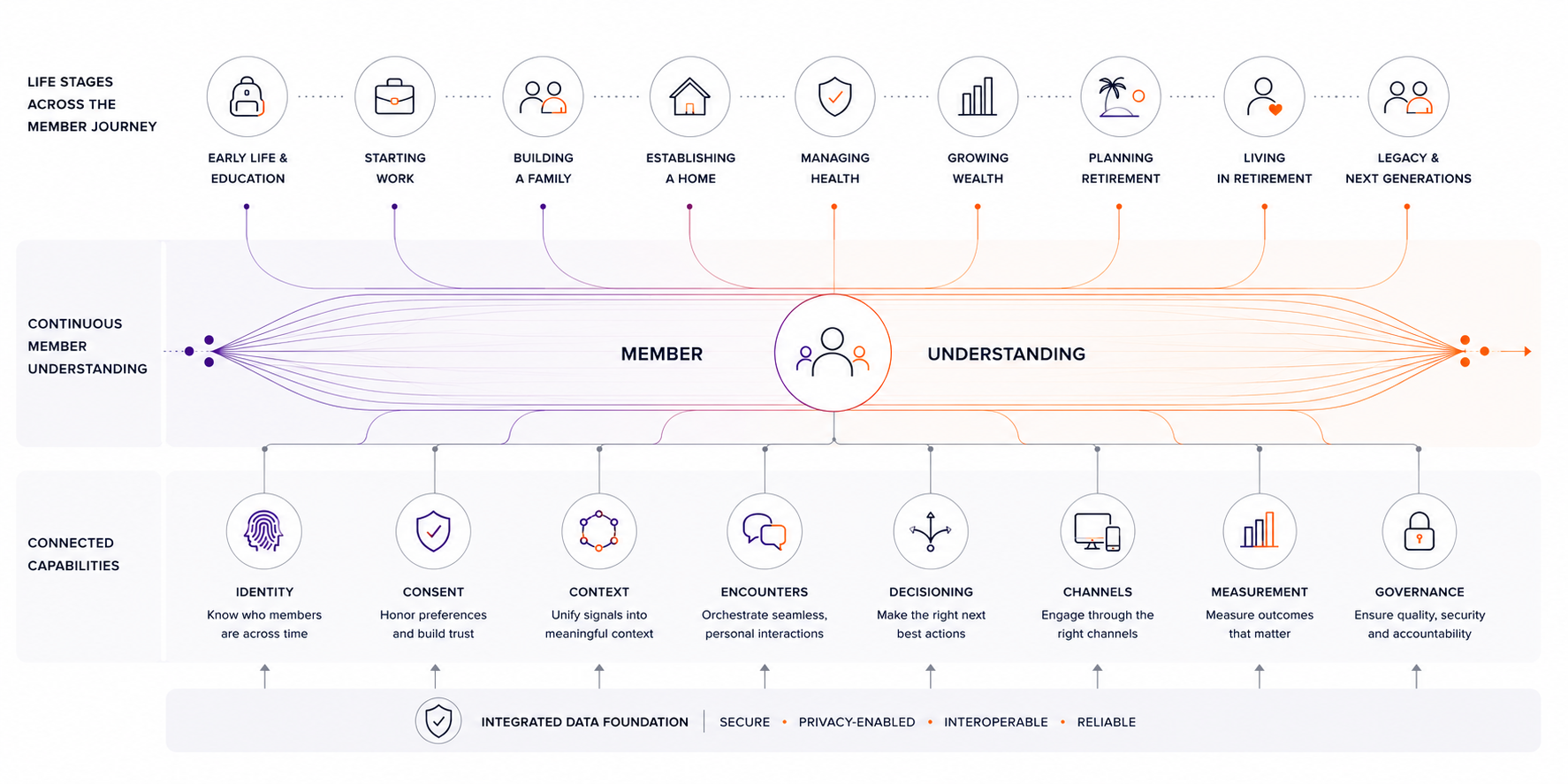

This is why Encounter Anatomy belongs at the centre of Customer Technology. The Mini MBA in Customer Technology already recognises this by including Encounter Anatomy, Hyperconnected Encounters, Engagement Fabric, Customer-Oriented Architecture, and Governance as core areas within the course’s structure. That sequence is important because it moves technology thinking away from isolated systems and toward the architecture of relationship events, continuity, scale, and control.

The encounter is where institutional intent meets human circumstance. If that encounter is poorly structured, the institution cannot learn responsibly. If it is well structured, every interaction becomes part of a governed system of understanding.

The Engagement Fabric

The answer to fragmented member technology is not simply another platform.

This is a critical point because technology markets often present architecture problems as product gaps. A new platform promises a single view. A new AI layer promises intelligence. A new journey tool promises orchestration. A new data environment promises insight. A new CRM promises relationship management. These tools may be valuable, but no single product can substitute for architectural coherence.

Member institutions need an engagement fabric.

An engagement fabric is the connected architecture through which identity, context, consent, interaction history, decisioning, channels, service, measurement, and governance operate together. It is not defined by a vendor category. It is defined by the institution’s ability to carry relationship understanding across the environments in which members experience the organisation.

The fabric begins with identity. The institution must know who the member is across systems, channels, products, roles, and life stages. Identity is not merely a login credential or customer number. It is the anchor for relationship continuity.

The fabric requires consent and permission management. Member institutions operate in sensitive domains. They cannot responsibly reuse context unless they know what is permitted, for what purpose, in which channel, under what regulatory constraints, and with what level of member understanding.

The fabric requires context. It must preserve relevant relationship knowledge across encounters without becoming intrusive or careless. Context needs structure, governance, lifecycle management, and interpretation.

The fabric requires interaction memory. Members should not have to rebuild the relationship from scratch each time they engage. Staff and systems should not operate blindly when meaningful history exists and can be used appropriately.

The fabric requires decisioning. Institutions need clear logic for how they decide what to communicate, recommend, escalate, suppress, prioritise, or hand over to human support. Decisioning cannot be left entirely to campaigns, workflows, or algorithms disconnected from member outcomes.

The fabric requires channel coordination. Members experience the institution across many surfaces. A message in one channel can affect trust in another. A service failure can undermine a campaign. A digital interaction can create a need for human support. Channels must be coordinated around relationship state, not merely optimised separately.

The fabric requires measurement. Institutions must measure more than activity and satisfaction. They need to understand whether interactions are strengthening confidence, reducing effort, improving outcomes, preserving trust, and lowering the cost of responsible service over time.

The fabric requires governance. Privacy, consent, fairness, vulnerability, audit, explainability, escalation, and compliance must be built into the operating architecture. They cannot be appended after systems are already acting.

A mature engagement fabric allows member institutions to move from fragmented activity to coherent stewardship. It gives technology leaders a way to think beyond applications and toward capability. It also gives executive leaders a way to understand why technology architecture is not merely an internal matter. It shapes how the institution behaves.

AI as an Architectural Stress Test

AI is not the centre of the Customer Technology problem, but it is making the problem harder to ignore.

Member institutions were already struggling with fragmented context, inconsistent data, disconnected journeys, weak identity resolution, channel silos, and governance complexity before the current wave of AI capability. AI does not create these problems. It exposes and amplifies them.

As AI enters service, communication, analytics, advice support, claims, operations, knowledge management, personalisation, and decisioning environments, the quality of the architecture beneath it becomes more consequential. Intelligent systems draw their usefulness from the context they can access, the permissions they must respect, the histories they can interpret, the rules that constrain them, and the evidence they can produce after acting.

Where the architecture is coherent, AI may extend stewardship. It may help staff understand member context more quickly. It may summarise history, detect patterns, support service quality, improve accessibility, identify emerging needs, reduce administrative burden, and make institutional knowledge more usable. It may help members navigate complexity and help institutions scale support responsibly.

Where the architecture is fragmented, AI may automate misunderstanding.

It may generate confident responses from incomplete data. It may personalise communications without adequate context. It may blur the boundary between education and advice. It may miss vulnerability signals. It may treat members inconsistently across channels. It may make recommendations based on stale or poorly governed information. It may create outputs that are difficult to audit. It may accelerate decisions without improving judgement.

This is why AI readiness is not primarily a model-selection problem. It is an architecture-of-understanding problem.

Technology leaders are under understandable pressure to demonstrate AI progress. Boards want productivity. Executives want cost reduction. Service leaders want automation. Marketing leaders want relevance. Risk leaders want control. Members want clearer support. Vendors offer copilots, bots, agents, decision engines, and generative interfaces. The pressure to move is real.

But in member institutions, AI capability must be evaluated through the lens of relationship stewardship. What context is the system using? Is that context accurate, current, and permitted? What kind of decision or suggestion is being made? Is the interaction service, education, advice, marketing, risk management, or something else? Can the institution explain the output? Can it audit the encounter? Can it escalate appropriately? Can it detect when a human should intervene? Can it avoid over-personalisation or inappropriate inference? Can it protect vulnerable members? Can it measure whether the use of AI improves member outcomes rather than merely reducing cost?

These are not questions for an AI policy document alone. They are Customer Technology questions.

AI will make strong architectures more valuable and weak architectures more dangerous. It increases the speed, scale, and confidence with which institutions act on whatever they understand or misunderstand. That makes Customer Technology discipline more urgent, not less.

Governance Is Part of the Architecture

In member institutions, governance cannot remain downstream from technology.

Too often, governance is treated as review, approval, compliance, risk assessment, or policy oversight applied after systems have been designed. That model is increasingly inadequate. When technology shapes member interactions, governs context, automates decisions, personalises communication, routes service, and supports AI, governance must be embedded within the architecture itself.

Consent is not merely a legal artefact. It is an operational condition that should determine what systems can do. Privacy is not merely a policy statement. It is a design constraint. Fairness is not merely an aspiration. It must influence decisioning, measurement, and monitoring. Vulnerability is not merely a service consideration. It must be recognisable within governed interaction pathways. Explainability is not merely a reporting requirement. It must be supported by traceable data, logic, and encounter records. Auditability is not merely a retrospective exercise. It must be designed into how systems act.

This is especially important for member-based institutions because their responsibilities are long-term and trust-sensitive. Members may not fully understand the systems acting around them. They may not know what data is held, how it is interpreted, what inferences are made, or how decisions are shaped. This asymmetry creates an obligation for restraint and clarity.

Governance must therefore operate at several levels.

It must govern data: quality, lineage, access, sensitivity, retention, and use. It must govern identity: who the member is, how records are matched, and how errors are corrected. It must govern consent: what permissions exist, how they are captured, and how they are enforced. It must govern context: which interpretations are valid, which are inferred, and which require caution. It must govern decisioning: what actions can be automated, recommended, suppressed, escalated, or personalised. It must govern channels: how messages, service, and support remain consistent across surfaces. It must govern AI: what models can do, what they cannot do, how outputs are reviewed, and how risk is monitored. It must govern measurement: what outcomes matter and how unintended consequences are detected.

This is why Customer Technology requires enterprise-level leadership. It sits across technology, data, risk, service, digital, marketing, operations, legal, compliance, and strategy. No single function can own the relationship architecture alone.

The institution needs shared principles, clear decision rights, and a common language for how technology should act in relation to members.

Without that governance, technology estates become collections of local optimisations. Each function improves its own performance, while the member relationship remains fragmented. Marketing optimises engagement. Service optimises resolution. Digital optimises conversion. Operations optimises throughput. Risk optimises control. Data optimises models. Technology optimises platforms. But the member experiences the combined effect.

Customer Technology governance exists to ensure that combined effect is coherent, responsible, and aligned with institutional purpose.

Customer Technology and the Future of Institutional Capability

The need for Customer Technology becomes clearer when viewed as a capability question rather than a systems question.

A member institution needs the capability to recognise members across contexts. It needs the capability to preserve relevant memory. It needs the capability to understand intent and life stage responsibly. It needs the capability to govern consent and sensitive information. It needs the capability to coordinate channels. It needs the capability to distinguish service, education, advice, marketing, and stewardship. It needs the capability to learn from encounters. It needs the capability to scale support without losing judgement. It needs the capability to use AI safely. It needs the capability to measure whether technology is strengthening or weakening the member relationship.

These capabilities may require platforms, but they are not created by platforms alone.

They require architecture, operating models, data discipline, governance, measurement, leadership, and professional knowledge. They require people who can understand both technology and member relationships. They require enterprise architects who understand customer systems, data leaders who understand relationship context, digital leaders who understand institutional trust, marketing leaders who understand governance, service leaders who understand longitudinal journeys, and executives who understand technology as a strategic condition of member outcomes.

This is why vendor training and implementation capability are insufficient. Member institutions do need people who know how to configure tools, integrate systems, analyse data, and deliver digital experiences. But they also need leaders capable of asking deeper architectural questions.

What is the member model? What is the institution’s theory of relationship continuity? What encounters matter? What context should persist? What permissions govern action? What constitutes responsible personalisation? How should relationship state be measured? Which decisions can be automated? Which require human judgement? How does technology support fiduciary or member-first obligations? How does the architecture reduce marginal cost while improving trust? How does the institution know whether its systems are creating understanding or merely producing activity?

These questions define a field.

The Mini MBA in Customer Technology is positioned around this need for formal management of customer technology, moving beyond simple vendor certification toward independent, evidence-based learning. Its course structure includes information theory, modelling systems, enterprise architecture, the tension between customer technology and marketing technology, engagement fabric, encounter anatomy, hyperconnected encounters, scaled capability, customer-oriented architecture, and governance. That breadth is important because the problem itself is not narrow. It spans communication, systems, architecture, interaction, scale, ethics, and institutional control.

For member-based institutions, this kind of capability is likely to become increasingly important. The organisations that mature in Customer Technology will be better positioned to turn scale into leverage, data into context, encounters into learning, AI into support, governance into trust, and digital infrastructure into relationship stewardship.

Those that do not may still appear technologically advanced. They may have modern platforms, attractive interfaces, and ambitious AI pilots. But without coherent architecture, they may continue to struggle with fragmentation, cost, inconsistency, weak member understanding, and limited capacity to act responsibly at scale.

The Architecture Beneath Stewardship

Member-based institutions are entering a period in which their technology architectures will become increasingly visible through their behaviour.

Members may not see the data models, integrations, consent structures, encounter records, decision engines, workflow rules, or governance controls beneath the surface. But they will experience their consequences. They will feel whether the institution remembers or forgets. They will notice whether interactions are coherent or repetitive. They will sense whether communications are relevant or generic. They will encounter the difference between support that understands context and service that merely processes requests. They will experience whether digital systems reduce burden or transfer complexity back to them.

Boards and executives will also experience the consequences. They will see whether technology reduces marginal cost or increases operating drag. They will see whether AI can be deployed responsibly or remains trapped in pilot mode. They will see whether member insight improves strategic decisions or remains fragmented across reports. They will see whether governance becomes easier because architecture supports it, or harder because controls must be manually imposed on systems never designed for stewardship.

The future of member institutions will not be determined by technology adoption alone. Adoption is now table stakes. The deeper question is whether technology has been architected around the human relationships these institutions exist to sustain.

That question is especially important because member-based organisations carry obligations that extend beyond service efficiency or commercial performance. They steward retirement security, financial resilience, healthcare access, insurance protection, community participation, professional identity, and collective trust. Their technology architectures are therefore not merely internal operating environments. They are part of the infrastructure through which social and economic security is delivered.

A member institution cannot steward what its architecture cannot understand.

This is why Customer Technology deserves recognition as a formal discipline. It gives leaders a way to move beyond platform accumulation, channel optimisation, and fragmented digital transformation toward the architecture of member understanding. It asks how institutions recognise, remember, interpret, govern, and act in relation to members over time. It connects technology economics to member outcomes. It treats scale as something to be designed, not merely possessed. It places governance inside architecture. It recognises AI as a powerful capability that depends on the quality of the context beneath it.

The next generation of leading member institutions will not simply be those with the largest asset bases, the best apps, the most data, or the most ambitious AI programs. They will be those capable of building coherent, governed, scalable architectures of member understanding.

That is the work of Customer Technology.

.png)

Join the next intake and start learning

September 7th, 2026